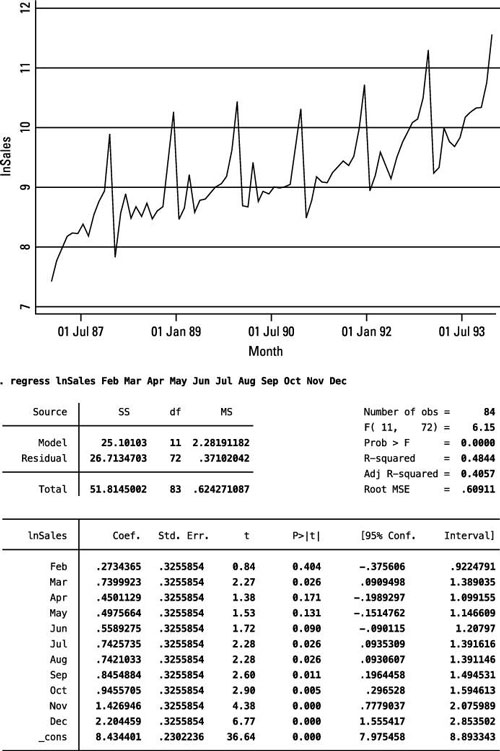

Seasonality effects can be correlated with both your dependent and independent variables. In order to avoid confounding the seasonality effects with those of your independent variables, you need to explicitly control for the season in which the measurement is observed.

If you include dummy variables for seasons along with the other relevant independent variables, you can simultaneously obtain better estimates of both seasonality and the effects of the other independent variables.

Consider the model

for a situation in which you believe that X directly causes Y. If, however, both X and Y are affected by seasonal trends for reasons unrelated to the relationship they have with each other, then X appears to have a strong effect on Y.

If seasonality significantly explains variation in the dependent variable and is also correlated with your independent variable, then you’ve excluded relevant variables from your model and have introduced bias into your estimated coefficients.

Adding season dummy variables to your regression allows you to pick up the seasonal co-movement of your variables and therefore make more convincing arguments about the causal relationship between your independent variables (Xs) and dependent variable (Y).

If you have a situation where seasonal effects are likely, then you should estimate a model like

where X represents your independent variable and S is your season dummy variable.