There are the basic steps in virtually every bookkeeping system. The steps are done in a particular order, although the methods by which the steps are done vary from business to business.

For example, entering the details of a sale can be done by scanning bar codes in a grocery store, or could require an in-depth legal interpretation for a complex order from a customer for an expensive piece of equipment.

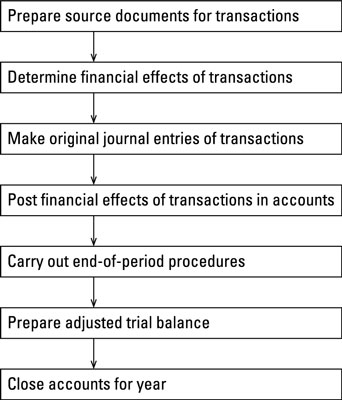

Prepare source documents for all transactions, operations, and other events of the business; source documents are the starting point in the bookkeeping process.

When buying products, a business gets a purchase invoice from the supplier. When borrowing money from the bank, a business signs a note payable, a copy of which the business keeps. When a customer uses a credit card to buy the business’s product, the business gets the credit card slip as evidence of the transaction. When preparing payroll checks, a business depends on salary rosters and time cards.

All of these key business forms serve as sources of information into the bookkeeping system — in other words, information the bookkeeper uses in recording the financial effects of the activities of the business.

Determine the financial effects of the transactions, operations, and other events of the business.

The activities of the business have financial effects that must be recorded — the business is better off, worse off or at least “different off as the result of its transactions. Examples of typical business transactions include paying employees, making sales to customers, borrowing money from the bank, and buying products that will be sold to customers.

The bookkeeping process begins by determining the relevant information about each transaction. The chief accountant of the business establishes the rules and methods for measuring the financial effects of transactions. Of course, the bookkeeper should comply with these rules and methods.

Make original entries of financial effects in journals, with appropriate references to source documents.

Using the source documents, the bookkeeper makes the first, or original, entry for every transaction into a journal; this information is later posted in accounts. A journal is a chronological record of transactions in the order in which they occur — like a very detailed personal diary.

Post the financial effects of transactions to accounts, with references to and tie-ins to original journal entries.

Only the official, established chart, or list of accounts, should be used in recording transactions. An account is a separate record, or page as it were, for each asset, each liability, and so on. One transaction affects two or more accounts. The journal entry records the whole transaction in one place; then each piece is recorded in the accounts that are affected by the transaction.

Perform end-of-period procedures — the critical steps for getting the accounting records up-to-date and ready for the preparation of management accounting reports, tax returns, and financial statements.

A period is a stretch of time — from one day to one month to one quarter (three months) to one year — that is determined by the needs of the business. A year is the longest period of time that a business would wait to prepare its financial statements. Most businesses need accounting reports and financial statements at the end of each quarter, and many need monthly financial statements.

The accountant needs to be heavily involved in end-of-period procedures and be sure to check for errors in the business’s accounts. Ideally, accounts should contain very few errors at the end of the period, but the accountant can’t make any assumptions and should make a final check for any errors that may have fallen through the cracks.

Compile the adjusted trial balance for the accountant, which is the basis for preparing management reports, tax returns, and financial statements.

After all the end-of-period procedures have been completed, the bookkeeper compiles a comprehensive listing of all accounts, which is called the adjusted trial balance. The accountant takes the adjusted trial balance and telescopes similar accounts into one summary amount that is reported in a financial report or tax return.

For example, a business may keep hundreds of separate inventory accounts, every one of which is listed in the adjusted trial balance. The accountant collapses all these accounts into one summary inventory account that is presented in the balance sheet of the business. In grouping the accounts, the accountant should comply with established financial reporting standards and income tax requirements.

Close the books — bring the bookkeeping for the fiscal year just ended to a close and get things ready to begin the bookkeeping process for the coming fiscal year.

Books is the common term for a business’s complete set of accounts. A business’s transactions are a constant stream of activities that don’t end tidily on the last day of the year, which can make preparing financial statements and tax returns challenging.

The business has to draw a clear line of demarcation between activities for the year (the 12-month accounting period) ended and the year yet to come by closing the books for one year and starting with fresh books for the next year.

Most medium-size and larger businesses have an accounting manual that spells out in great detail the specific accounts and procedures for recording transactions. A business should regularly review its chart of accounts and accounting rules and policies and make revisions.

Companies do not take this task lightly; discontinuities in the accounting system can be major shocks and have to be carefully thought out. Nevertheless, bookkeeping and accounting systems can’t remain static for very long. If these systems were never changed, bookkeepers would still be sitting on high stools making entries with quill pens and bottled ink in leather-bound ledgers.