When your business first receives inventory, you enter the initial cost of that inventory into the bookkeeping system based on the shipment’s invoice. Invoices are sometimes sent separately, and only a packing slip is included in the order. If that’s the case, you should still record the receipt of the goods because the company incurs the cost from the day the goods are received.

The company must be sure it will have the money to pay for the goods when the invoice arrives and the bill comes due. You track outstanding bills in the Accounts Payable account.

Entering inventory transactions manually

Entering the receipt of inventory is a relatively easy entry in the bookkeeping system. For example, if your company buys $1,000 of inventory to be sold, you make the following record in the books:

| Account | Debit | Credit |

|---|---|---|

| Purchases | $1,000 | |

| Accounts Payable | $1,000 |

The Purchases account increases by $1,000 to reflect the additional costs, and the Accounts Payable account increases by the same amount to reflect the amount of the bill that needs to be paid in the future.

When inventory enters your business, in addition to recording the actual costs, you need more detail about what was bought, how much of each item was bought, and what each item cost. You also need to track:

How much inventory you have on hand.

The value of the inventory you have on hand.

When you need to order more inventory.

Tracking these details for each type of product bought can be a nightmare, especially if you’re trying to keep the books for a retail store because you need to set up a special Inventory journal with pages detailing purchase and sale information for every item you carry.

Entering inventory transactions by computer

Computerized accounting simplifies this process of tracking inventory. Details about inventory can be entered initially into your computer accounting system in several ways:

If you pay by check or credit card when you receive the inventory, you can enter the details about each item on the check or credit card form.

If you use purchase orders, you can enter the detail about each item on the purchase order, record receipt of the items when they arrive, and update the information when you receive the bill.

If you don’t use purchase orders, you can enter the detail about the items when you receive them and update the information when you receive the bill.

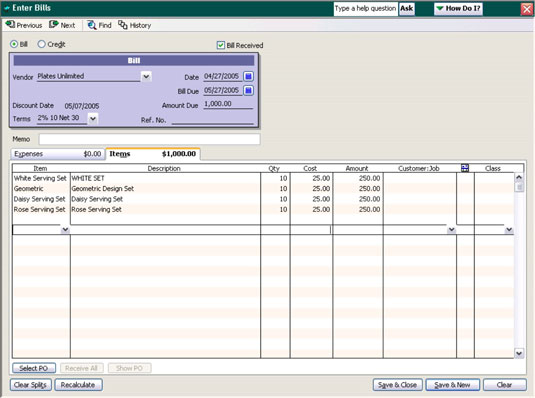

To give you an idea of how this information is collected in a computerized accounting software program, the following figure shows you how to enter the details in QuickBooks. This particular form is for the receipt of inventory with a bill, but similar information is collected on the software program’s check, credit card, and purchase order forms.

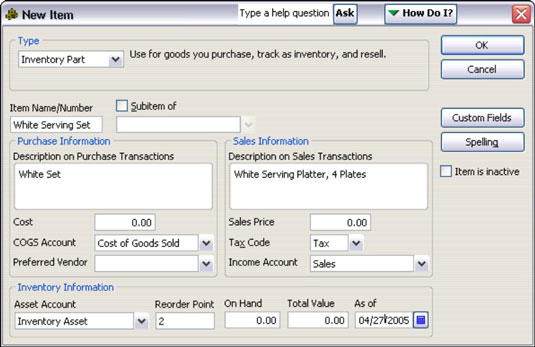

The next figure shows how you initially set up an inventory item in the computerized accounting system. Note that in addition to the item name, two descriptions are added to the system: One is an abbreviated version you can use on purchase transactions, and the other is a longer description that shows on customer invoices (sales transactions). You can input a cost and sales price if you want, or you can leave them at zero and enter the cost and sales prices with each transaction.

If you have a set contract purchase price or sales price on an inventory item, it saves time to enter it on this form so you don’t have to enter the price each time you record a transaction. But, if the prices change frequently, it’s best to leave the space blank so you don’t forget to enter the updated price when you enter a transaction.

Notice in the preceding figure that information about inventory on hand and when inventory needs to be reordered can also be tracked using this form. To be sure your store shelves are never empty, for each item you can enter a number that indicates at what point you want to reorder inventory.

After you complete and save the form that records the receipt of inventory in QuickBooks, the software automatically:

Adjusts the quantity of inventory you have in stock

Increases the asset account called Inventory

Lowers the quantity of items on order (if you initially entered the information as a purchase order)

Averages the cost of inventory on hand

Increases the Accounts Payable account