Managerial Accounting For Dummies Cheat Sheet

Managerial accounting provides managers and other decision-makers with financial information about their companies so managers understand how much their products cost, how their companies make money, and how to plan for future profits and growth. To use this information profitably, managers and decision-makers must understand the many terms managerial accountants use.

When planning for the future, managers and decision-makers follow a master budgeting process. To prepare this budget, and to understand how costs behave, managers and decision-makers should understand cost-volume-profit relationships, which explain how changes in volume or price impact profits.

Key costs related to managerial accounting

In accounting, a cost measures how much you pay/sacrifice for something. Managerial accounting must give managers accurate cost information relevant to their management decisions. Here are several cost-related terms you encounter in managerial accounting:

- Direct cost: Cost that you can trace to a specific product

- Indirect cost: Cost that you can’t easily trace to a specific product

- Materials: Physical things you need to make products

- Labor: Work needed to make products

- Overhead: Indirect materials, indirect labor, and other miscellaneous costs needed to make products

- Variable costs: Costs that change in direct proportion with activity level

- Fixed costs: Costs that don’t change with activity level

- Mixed costs: Combination of fixed and variable costs

- Contribution margin: Sales less variable costs

- Product costs: Costs needed to make goods; considered part of inventory until sold

- Period costs: Costs not needed to make goods; recorded as expenses when incurred

- Work-in-process cost: How much you paid for goods that are started but not yet completed

- Finished goods cost: How much you paid for goods completed but not yet sold

- Cost of goods manufactured: The cost of the goods completed during a period

- Cost of goods sold: The cost of making goods that you sold

- Controllable costs: Costs that you can change

- Noncontrollable costs: Costs that you can’t change

- Conversion costs: Direct labor and overhead

- Incremental costs: Costs that change depending on which alternative you choose; also known as relevant costs and marginal costs

- Irrelevant costs: Costs that don’t change depending on which alternative you choose

- Opportunity costs: Costs of income lost because you chose a different alternative

- Sunk costs: Costs you’ve already paid or committed to paying

- Historical cost: How much you originally paid for something

- Cost per unit: Cost of a single unit of product

- Expense: Costs deducted from revenues on the income statement

- Cost driver: Factor thought to affect costs

- Process cost: Cost of similar goods made in large quantities on an assembly line

- Job order cost: Cost of a batch of specially made goods

- Absorption cost: Cost that includes fixed and variable product costs

- Target cost: Cost goal set for engineers designing a product

Budgets that go into creating a master budget

A master budget is a plan created to manage a company’s manufacturing and sales activity to meet profit and cash flow goals. Creating a master budget requires careful coordination of several smaller budgets covering all parts of the organization; that way, the master budget is realistic but not complacent. The master budget contains the following elements:

- Sales budget

- Production budget

- Direct materials budget

- Direct labor budget

- Manufacturing overhead budget

- Selling and administrative budget

- Capital acquisitions budget

- Cash budget

- Budgeted financial statements

Cost-volume-profit relationships for managerial accounting

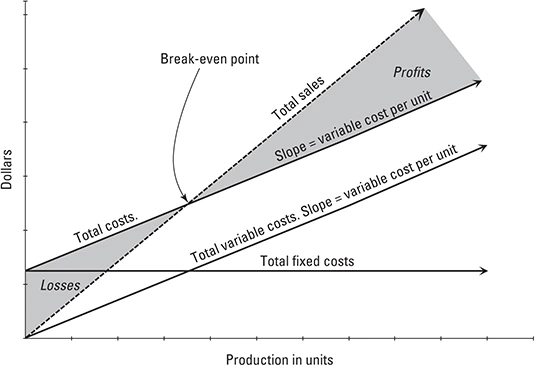

Managerial accounting provides useful tools, such as cost-volume-profit relationships, to aid decision-making. Cost-volume-profit analysis helps you understand different ways to meet your company’s net income goals. This figure describes the relationship among sales, fixed costs, variable costs, and net income.

The bottom axis indicates the level of production — the number of units you make. The left axis indicates value in dollars.

Where total sales equals total costs, the company breaks even (which is why that’s called the break-even point). The shaded area to the upper right of this break-even point is profit. The shaded region to the lower left is net loss. Total variable costs are a diagonal line because the higher the production, the greater the variable costs. The total fixed costs line is horizontal because regardless of the production level, fixed costs stay the same. Total costs equal the sum of total variable costs and total fixed costs.

About This Article

This article can be found in the category:

Hot off the press

Explore Related content