Finally, that wonderful day comes when the debt is paid off. You may not think of it as a thorny accounting situation — and it isn’t, as long as the debt is held to maturity. In other words, there’s no problem as long as the debtor doesn’t pay it off early.

However, if an event occurs that leads a company to pay off debt (whether a note or a bond) early, the company may have to figure gain or loss on the transaction. The regular amortization journal entries did not zero out any discount or premium on the debt payable.

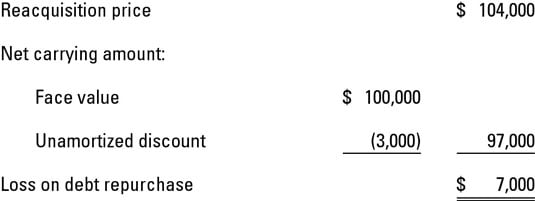

If the acquisition price is greater than the carrying value of the debt, there’s a loss on extinguishment. A gain occurs if the acquisition price is less than the carrying value.

A good example of how gain may occur is the accounting for callable debt, which means the issuer can pay off the debt before the maturity date. In the business world, this scenario happens if the interest rate falls and it’s possible to reissue the debt at 6 percent. This situation is often referred to as the debt being callable.

Need an example on the accounting for the early extinguishment of debt?

Imagine that a company repurchases a note payable for $104,000 whose face value was $100,000. It was issued at a discount, of which $3,000 isn’t yet amortized at the date of repurchase. Gain or loss on the transaction?

Remember that a business can remove the debt from its balance sheet only if one of the following occurs:

The debtor pays the creditor and is totally relieved of the obligation. For example, the debt was for $10,000 and the debtor paid the creditor the full $10,000 plus all required interest.

The creditor legally releases the debtor from any further obligation. For example, the creditor agrees to cancel a portion of the debt.

Troubled debt restructuring is an advanced financial accounting topic. This takes place when there are market or legal reasons why terms of the debt are modified. A good example of this when the financial institution lowers the interest rate they are charging the business for the debt.

On the personal side, you may have had friends participating in a residential short sale, which means a house is sold for less than the mortgage debt still owed on it with the lender taking a loss on the sale.