A direct labor variance is caused by differences in either wage rates or hours worked. As with direct materials variances, you can use either formulas or a diagram to compute direct labor variances.

Utilizing formulas to figure out direct labor variances

To estimate how the combination of wages and hours affects total costs, compute the total direct labor variance. As with direct materials, the price and quantity variances add up to the total direct labor variance.

To compute the direct labor price variance (also known as the direct labor rate variance), take the difference between the standard rate (SR) and the actual rate (AR), and then multiply the result by the actual hours worked (AH):

Direct labor price variance = (SR – AR) x AH

To get the direct labor quantity variance (also known as the direct labor efficiency variance), multiply the standard rate (SR) by the difference between total standard hours (SH) and the actual hours worked (AH):

Direct labor quantity variance = SR x (SH – AH)

The direct labor variance equals the difference between the total budgeted cost of labor (SR x SH) and the actual cost of labor, based on actual hours worked (AR x AH):

Total direct labor variance = (SR x SH) – (AR x AH)

Now you can plug in the numbers for the Band Book Company. Band Book’s direct labor standard rate (SR) is $12 per hour. The standard hours (SH) come to 4 hours per case. Because Band made 1,000 cases of books this year, employees should have worked 4,000 hours (1,000 cases x 4 hours per case). However, employees actually worked 3,600 hours, for which they were paid an average of $13 per hour.

With these numbers in hand, you can apply the formula to compute the direct labor price variance:

Direct labor price variance = (SR – AR) x AH = ($12.00 – $13.00) x 3,600 = –$1.00 x 3,600 = –$3,600 unfavorable

According to the direct labor price variance, the increase in average wages from $12 to $13 cause costs to increase by $3,600. Now plug the numbers into the formula for the direct labor quantity variance:

Direct labor quantity variance = SR x (SH – AH) = $12.00 x (4,000 – 3,600) = $12.00 x 400 = $4,800 favorable

Employees worked fewer hours than expected to produce the same amount of output. This change saves the company $4,800 — a favorable variance. To compute the total direct labor variance, use the following formula:

Total direct labor variance = (SR x SH) – (AR x AH) = ($12.00 x 4,000) – ($13.00 x 3,600) = $48,000 – $46,800 = $1,200 favorable

According to the total direct labor variance, direct labor costs were $1,200 lower than expected, a favorable variance.

Employing diagrams to work out direct labor variances

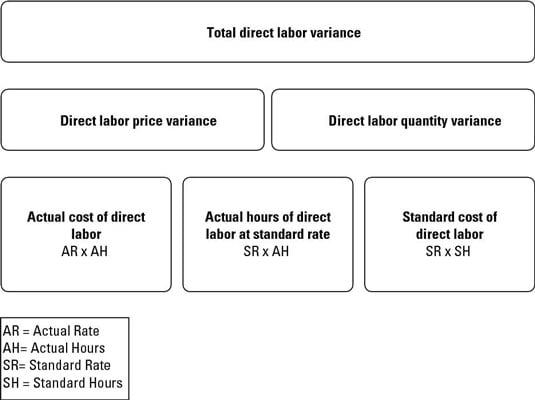

The figure shows you how to use a diagram to compute price and quantity variances quickly and easily. First, compute the totals in the third row: actual cost, actual hours at standard rate, and the standard cost. To get the direct labor price variance, subtract the actual cost from the actual hours at standard.

The difference between the standard cost of direct labor and the actual hours of direct labor at standard rate equals the direct labor quantity variance. The total of both variances equals the total direct labor variance.

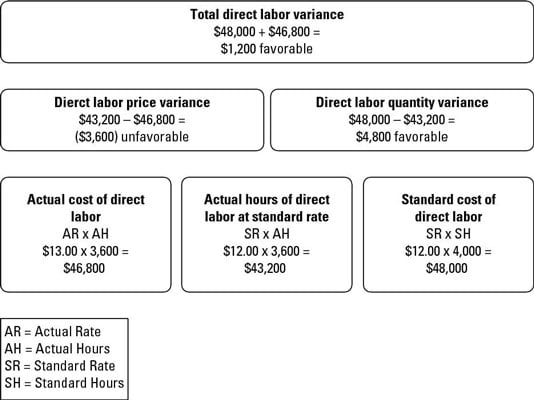

Take a look at the next figure to see this diagram in action for Band Book: Starting from the bottom, the actual cost of direct labor amounts to $46,800. The actual hours of direct labor at standard rate equals $43,200. The standard cost of direct labors comes to $48,000.

To compute the direct labor price variance, subtract the actual hours of direct labor at standard rate ($43,200) from the actual cost of direct labor ($46,800) to get a $3,600 unfavorable variance. This result means the company incurs an additional $3,600 in expense by paying its employees an average of $13 per hour rather than $12.

To compute the direct labor quantity variance, subtract the standard cost of direct labor ($48,000) from the actual hours of direct labor at standard rate ($43,200). This math results in a favorable variance of $4,800, indicating that the company saves $4,800 in expenses because its employees work 400 fewer hours than expected.

The $1,200 favorable variance arises because of two factors: the company saves $4,800 from fewer hours worked but incurs an additional $3,600 expense by paying its employees more money per hour than planned. This scenario begs the question “Are higher-paid workers more productive?” But that’s a discussion for the human resources experts.