When an accountant records a sale or expense entry using double-entry accounting, he or she sees the interconnections between the income statement and balance sheet. A sale increases an asset or decreases a liability, and an expense decreases an asset or increases a liability.

Therefore, one side of every sales and expense entry is in the income statement, and the other side is in the balance sheet. You can’t record a sale or an expense without affecting the balance sheet. The income statement and balance sheet are inseparable, but they aren’t reported this way!

To properly interpret financial statements, you need to understand the links between the statements, but the links aren’t easy to see. Each financial statement appears on a separate page in the annual financial report, and the threads of connection between the financial statements aren’t referred to.

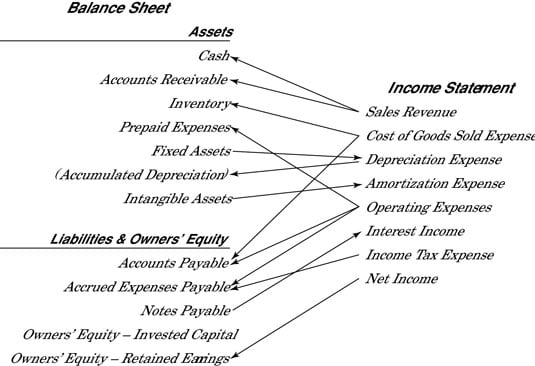

The following figure shows the lines of connection between income statement accounts and balance sheet accounts. When reading financial statements, in your mind’s eye, you should “see” these lines of connection. Because financial reports don’t offer a clue about these connections, it may help to actually draw the lines of connection, like you would if you were highlighting lines in a textbook.

Here’s a quick summary explaining the lines of connection in the figure, starting from the top and working down to the bottom:

Making sales (and incurring expenses for making sales) requires a business to maintain a working cash balance.

Making sales on credit generates accounts receivable.

Selling products requires the business to carry an inventory (stock) of products.

Acquiring products involves purchases on credit that generate accounts payable.

Depreciation expense is recorded for the use of fixed assets (long-term operating resources).

Depreciation is recorded in the accumulated depreciation contra account (instead decreasing the fixed asset account).

Amortization expense is recorded for limited-life intangible assets.

Operating expenses is a broad category of costs encompassing selling, administrative, and general expenses:

Some of these operating costs are prepaid before the expense is recorded, and until the expense is recorded, the cost stays in the prepaid expenses asset account.

Some of these operating costs involve purchases on credit that generate accounts payable.

Some of these operating costs are from recording unpaid expenses in the accrued expenses payable liability.

Borrowing money on notes payable causes interest expense.

A portion (usually relatively small) of income tax expense for the year is unpaid at year-end, which is recorded in the accrued expenses payable liability.

Earning net income increases retained earnings.