Businesses that manufacture products have several additional cost factors to consider compared with retailers and distributors. These types of manufacturing costs include raw materials, direct labor, variable overhead, and fixed overhead.

Manufacturing costs consist of four basic types:

Raw materials (also called direct materials): What a manufacturer buys from other companies to use in the production of its own products. For example, General Motors buys tires from Goodyear (or other tire manufacturers) that then become part of GM’s cars.

Direct labor: The employees who work on the production line.

Variable overhead: Indirect production costs that increase or decrease as the quantity produced increases or decreases. An example is the cost of electricity that runs the production equipment: You pay for the electricity for the whole plant, not machine by machine, so you can’t attach this cost to one particular part of the process.

But if you increase or decrease the use of those machines, the electricity cost increases or decreases accordingly. (In contrast, the monthly utility bill for a company’s office and sales space probably is fixed for all practical purposes.)

Fixed overhead: Indirect production costs that do not increase or decrease as the quantity produced increases or decreases. These fixed costs remain the same over a fairly broad range of production output levels. Three significant fixed manufacturing costs are:

Salaries for certain production employees who don’t work directly on the production line, such as a vice president, safety inspectors, security guards, accountants, and shipping and receiving workers.

Depreciation of production buildings, equipment, and other manufacturing fixed assets.

Occupancy costs, such as building insurance, property taxes, and heating and lighting charges.

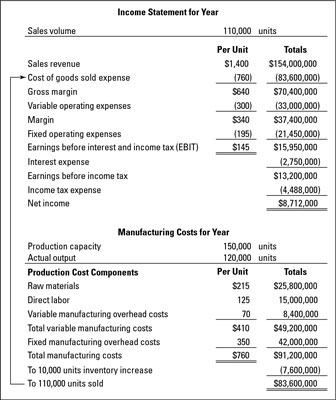

The figure below presents an annual income statement for a manufacturer and includes information about its manufacturing costs for the year. The cost of goods sold expense depends directly on the product cost from the summary of manufacturing costs that appears below the income statement.

A business may manufacture 100 or 1,000 different products, or even more, and the business must prepare a summary of manufacturing costs for each product. To keep our example easy to follow (but still realistic), the figure presents a scenario for a one-product manufacturer. This example illustrates the fundamental accounting problems and methods of all manufacturers.

The information in the manufacturing costs summary below the income statement (see the figure above) is highly confidential and for management eyes only. Competitors would love to know this information. A company may enjoy a significant cost advantage over its competitors and definitely does not want its cost data to get into their hands.