How do you define financial wealth or financial independence? Someone who has accumulated an asset base that allows them to live off that asset base for life.

The definition implies a passive income earning position. It implies that no work, or no additional income, is required to maintain a specific lifestyle. When you strip all the flowery language away, it really boils down to a number. We are going to start with that premise.

The question is, what’s your number?

There are a number of strategies you can employ to arrive at your number. Each of these that we explore has merit and value. The true question is, which of these speaks and motivates you?

Earning replacement income

The first method is to focus on the replacement of income. The goal would be to acquire enough income-producing assets to replace all, or a part, of your current earnings. What is the amount of money you need to acquire to replace your present-day income, plus a factor for inflation. The goal is to buy enough bonds, annuities, pension payments, dividend stocks, real estate, and mortgage notes that create a cash flow to cover your expenses. This is certainly a viable way to create a number that you craft a plan too. This plan creates a replaced income without reducing your asset base. It allows you to spend your income freely, knowing you have future safety as well.Setting a gross asset number

Another way to develop a wealth strategy is to calculate a gross asset number. What overall net worth number do you need where the income plus drawing on the asset will create years of income to fund your lifestyle? It gives you a very specific target, which allows you to plan as well as check your progress too. It becomes a simple math equation of lifestyle and length of life. You then apply a standard 4-percent rule to your net amount.The 4-percent rule has been around for years as a benchmark for retirees. This rule describes how much a retiree can withdraw each year in retirement while also retaining enough of an asset base in their account to last 30-plus years. So, if you have $1,000,000, you can draw out $40,000 per year and likely never run out of money. This rule is just a guide, so if your asset base drops due to a stock market crash, you might have to adjust.

Beware of being general, arbitrary, or having round ballpark numbers. My belief is that specificity creates attraction. The law of attraction states that you will be attracted to what you are looking for and what you desire. If you are specific, the power of the pull will be greater. As you march along to your specific goal, your intention, energy, and excitement will increase because you can clearly see the progress. The law of attraction is a powerful tool to the achievement of wealth.

Getting help from other sources

A good financial planner can really be invaluable in defining the number and factoring for inflation. If you want to go it alone in your calculation, Kiplinger has an easy-to-use retirement savings calculator. It will take you about ten minutes to work through it. It factors in the variables of time, returns, inflation, and years in retirement. You can include Social Security in the calculations or not.The objective is to give you a target. That target is reasonably accurate in what you need plus what you need to save on a regular basis for how many years you need before retirement. When you use the retirement savings calculator, be sure to adjust the timing, rates of return, and length of retirement. All those factors can influence significantly the nest egg number. You should play with the numbers. Create some variation so that you understand how different economic conditions might affect your results, or higher savings rates will affect the outcome, and so forth.

Deciding what you need

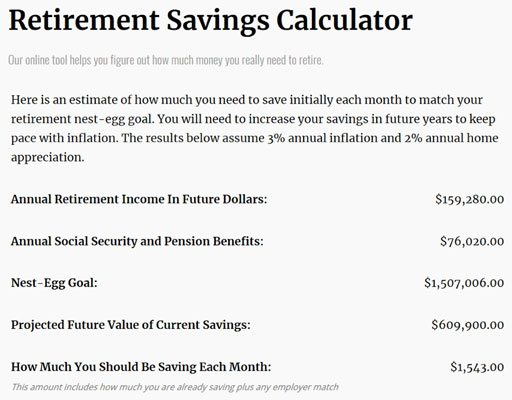

Take a look at the following image, in which the Retirement Savings Calculator is used. For some, a 1.5-million dollar nest egg goal seems big. For others, it might seem small. The $159,000 annual income goal in the figure is two and a half times the median income the United States currently. That’s not in the 1-percent income level, but it's certainly an upper-middle-class lifestyle in terms of annual income. The real question is, what do you need? Kiplinger's online retirement savings calculator is easy to use.

Kiplinger's online retirement savings calculator is easy to use.The $76,020 in Social Security income might also seem like a lot, but it’s only 47 percent of the overall income. The Social Security Administration quotes that Social Security is designed to replace about 40 percent of a person’s income in retirement.

In this example, the savings still needs to be at $1,543 per month toward retirement. According to Vanguard, about 12 percent of 401k plan participants contribute the maximum amount to their 401k plan each year. The present maximum level is $18,500 per year if you are under 50 years of age. If you are over 50, you are allowed another $6,000 for a total of $24,500. Interestingly, the $1,543 a month, would be achieved just by maxing out your 401k plan each year.

Most people want financial wealth or financial independence but have never even taken the 10 minutes to define what that number is. You can’t hit a target that you have not defined or aimed for.

The path is in the math

You have to do the math so that you can work effectively to craft your plan and set the strategy. Let’s look at a few more basic math calculations to check how you are doing. The goal is to give you a perspective of exactly where you need to be long term, as well as compare it to where you are right now. If you used the Kiplinger tool discussed in the preceding sections, you understand clearly where you need to be.A good financial plan is not really glamorous. It’s not exciting. What creates excitement is having the plan and starting the process to achieving it. A good plan works because it is just common sense combined with simple savings disciplines. It has savings targets and savings goals. For example, consider forced savings out of your paycheck. You decide to deduct $200 per paycheck and place the money in a savings account or a 401k.

The complex stuff makes for great conversations at cocktail parties. But the strategies of paying off non-deductible debt, forced savings, solid real estate cash flow investing, and compound interest don’t make for great conversation at cocktail parties, but they can eventually pay for great cocktail parties!

What is your current savings goal monthly? How does that relate to your needed goal of monthly savings you calculated? If it’s short, how much short is it? What steps in your family budget are you going to take to increase your savings? What extra work, overtime, or side jobs can you do to increase your monthly savings rate? What is a reasonable timeframe to achieve the increase in savings? You might not be able to do it now due to other debt you are paying off. That won’t sink your ship if you can eventually improve your position.

What is a reasonable timeframe to close any gaps that exist? You don’t have to make up the shortage this month, or even this year. If you, through a deliberate plan, close that gap in the next few years by even placing 100 percent of the raises or periodic side job earnings into savings, the fact that it took you a few years to reach your savings goal will likely be a non-event 30 years down the road in retirement.

The power of compound interest

The eighth wonder of the world is compound interest. “He who understands it, earns it. He who doesn’t, pays it,” stated Albert Einstein. Compound interest is one of your best friends in crafting a wealth plan.Compound interest is like a snowball that is traveling down a hill. It continues to pick up more snow, growing in size as it travels. That is the principle as well as the outcome of compound interest. Compound interest does all this work of growth automatically. It does it while you sleep. As long as your investment is paying you a return in interest, dividend, or rent, you reinvest those gains. The longer the timeframe, the wealthier you become. Time is actually your ally with compound interest.

If you start to save $5,000 a year at age 20, by age 60, in 40 years, you would have 2.4 million dollars. You would have saved a total of $200,000 in that 40 years. At 80 years old you would have 16.7 million by saving only $300,000 of income over 60 years. Look at the difference between ages 60 and 80. In 20 years, with only $100,000 added through savings, you went from 2.4 million to 16.7 million. It's astounding!

Net worth targets

There are a number of factors that influence your wealth and net worth. Net worth is defined by taking your assets and subtracting your liabilities to create a net asset number, or net worth number. If you sold everything you owned, paid off all your debts, and had money left over, that would be your net worth. Your net worth is one measure of how you are doing in your quest for financial independence and wealth.The net worth number can be influenced by a number of factors. Your income is certainly a factor, as well as your age. As you age, because you have been working more years, your net worth should be increasing. You also have more assets. You have cars, boats, furniture, and real estate. The home you own is likely one of the biggest influences on your net worth, but be careful. A home you own, rather than an apartment you rent, can help you increase net worth through the home’s appreciation, as well as paying down the mortgage debt each month.

Thomas Stanley wrote the landmark book, The Millionaire Next Door, one of the classic wealth books of our day. He describes a formula for checking your net worth based on your earnings and age. If you earn more, you should theoretically have a higher net worth. This formula gives you a simple way to check the math.

Net worth target wealth formula to success:

Age × Annual household income / 10 = net worth at ageThe following table gives you an example of how this formula works:

| Age | x | Annual Income | / | 10 | = | Net Worth |

| 35 | x | $250,000 | / | 10 | = | $875,000 |

| 35 | x | $100,000 | / | 10 | = | $350,000 |

| 36 | x | $50,000 | / | 10 | = | $175,000 |

This formula provides a gauge on how you are doing with your personal expenses, savings, and net worth. The largest portion of most people’s net worth in their 30s and 40s is likely the home they own. That is to be expected. When you reach your 50s and 60s, if that is still the case, you need to step up your savings, and fast.

Home ownership and net worth

A home that you own is a foundational building block to wealth. Unfortunately, too much of our net worth is attached to homeownership. We all saw the effect of the recent recession and housing crisis that hit in 2008. The net worth of so many people was devastated. We can get too attached to a home, and then we risk becoming house-rich and asset-poor.If your home presently is a significant portion of your net worth, that is fine for today. When that is not fine is ten-plus years from now. Your goal should be to change the influence of your home from a significant portion of your net worth to a small portion of your net worth. From being 60 to 80 percent of your net worth to over time being less than 20 percent of your net worth. I can hear it now: “But Dirk, my home is worth 400,000 dollars. That means I need a net worth of 2 million dollars.” That’s right!

It all boils down to one simple reason: You can’t spend your home. Your home doesn’t create income. It’s not an asset in classical terms. It doesn’t create income or return. Yes, it can appreciate in value and likely will. But you can’t spend that increase unless you mortgage it or sell it. You are not creating more assets from your home like you would stocks, bonds, mutual funds, or rental real estate assets. You will likely achieve appreciation in value of your home. The only way you can spend or live off that appreciation is to sell your home and downsize to a smaller home or lower standard of living. The truth is, few people do that in life. They might when their health requires it, but then they have expenses in an assisted-living facility.

Now there are folks who might sell the older home they raised their family in because it’s too large for them or the maintenance is too much. What happens most frequently is that they buy a smaller, newer home with more quality and amenities. They say, “I deserve a nicer home with new hardwood floors and custom cabinets. I want to be able to live on a golf course and have a three-car garage where I can park a golf cart.” That gap between their larger, older home and the new home is not as significant financially as they first imagined.

So, your home is part of your net worth, but it should not be a large factor in your asset base or nest egg calculations.