How about a new car? A trip to your friendly local car dealer shows you that a new set of wheels will set you back $25,000+. Although more people may have the money to pay for that than, say, the college education, what if you don’t? Should you finance the car the way you finance the education?

The auto dealers and bankers who are eager to make you an auto loan say that you deserve and can afford to drive a nice, new car, and they tell you to borrow away (or lease). I say, “No! No! No!” Why do I disagree with the auto dealers and lenders? For starters, I’m not trying to sell you a car or loan from which I derive a profit! More importantly, there’s a big difference between borrowing for something that represents a long-term investment and borrowing for short-term consumption.

If you spend, say, $1,500 on a vacation, the money is gone. Poof! You may have fond memories and photos, but you have nothing of financial value to show for it. “But,” you say, “vacations replenish my soul and make me more productive when I return … the vacation more than pays for itself!”I’m not saying that you shouldn’t take a vacation. By all means, take one, two, three, or as many vacations and trips as you can afford yearly. But the point is to take what you can afford. If you have to borrow money in the form of an outstanding balance on your credit card for many months in order to take the vacation, then you can’t afford it.

Consuming your way to bad debt

I coined the term bad debt to refer to debt incurred for consumption, because such debt is harmful to your long-term financial health. (I used this term back in the early 1990s when the first edition of this book was published, and I’m flattered that others have since used the same terminology.)You’ll be able to take many more vacations during your lifetime if you save the cash in advance. If you get into the habit of borrowing and paying all the associated interest for vacations, cars, clothing, and other consumer items, you’ll spend more of your future income paying back the debt and interest, leaving you with less money for your other goals.

The relatively high interest rates that banks and other lenders charge for bad (consumer) debt is one of the reasons you’re less able to save money when using such debt. Not only does money borrowed through credit cards, auto loans, and other types of consumer loans carry a relatively high interest rate, but it also isn’t tax-deductible.

I’m not saying that you should never borrow money and that all debt is bad. Good debt, such as that used to buy real estate and small businesses, is generally available at lower interest rates than bad debt and is usually tax-deductible. If well managed, these investments may also increase in value. Borrowing to pay for educational expenses can also make sense. Education is generally a good long-term investment because it can increase your earning potential. And student loan interest is tax-deductible, subject to certain limitations). Taking out good debt, however, should be done in proper moderation and for acquiring quality assets.

How to recognize bad debt overload

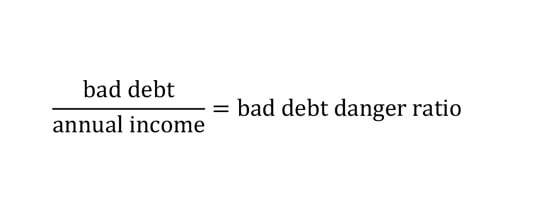

Calculating how much debt you have relative to your annual income is a useful way to size up your debt load. Ignore, for now, good debt — the loans you may owe on real estate, a business, an education, and so on. I’m focusing on bad debt, the higher-interest debt used to buy items that depreciate in value.To calculate your bad debt danger ratio, divide your bad debt by your annual income. For example, suppose you earn $40,000 per year. Between your credit cards and an auto loan, you have $20,000 of debt. In this case, your bad debt represents 50 percent of your annual income.

The financially healthy amount of bad debt is zero. While enjoying the convenience of credit cards, never buy anything with your credit card(s) that you can’t afford to pay off in full when the bill comes at the end of the month. Not everyone agrees with me. One major U.S. credit-card company says — in its “educational” materials, which it “donates” to schools to teach students about supposedly sound financial management — that carrying consumer debt amounting to 10 to 20 percent of your annual income is just fine.

When your bad debt danger ratio starts to push beyond 25 percent, it can spell real trouble. Such high levels of high-interest consumer debt on credit cards and auto loans grow like cancer. The growth of the debt can snowball and get out of control unless something significant intervenes.

How much good debt is acceptable? The answer varies. The key question is: Are you able to save sufficiently to accomplish your goals?Borrow money only for investments (good debt) — for purchasing things that retain and hopefully increase in value over the long term, such as an education, real estate, or your own business. Don’t borrow money for consumption (bad debt) — for spending on things that decrease in value and eventually become financially worthless, such as cars, clothing, vacations, and so on.

Assessing good debt: Can you get too much?

As with good food, you can get too much of a good thing, including good debt! When you incur debt for investment purposes — to buy real estate, for small business, even your education — you hope to see a positive return on your invested dollars.But some real-estate investments don’t work out. Some small businesses crash and burn, and some educational degrees and programs don’t help in the way that some people hope they will.

There’s no magic formula for determining when you have too much “good debt.” In extreme cases, I’ve seen entrepreneurs, for example, borrow up to their eyeballs to get a business off the ground. Sometimes this works, and they end up financially rewarded, but in most cases, extreme borrowing doesn’t.

Here are three important questions to ponder and discuss with your loved ones about the seemingly “good debt” you’re taking on:

- Are you and your loved ones able to sleep well at night and function well during the day, free from great worry about how you’re going to meet next month’s expenses?

- Are the likely rewards worth the risk that the borrowing entails?

- Are you and your loved ones financially able to save what you’d like to work toward your goals?

Playing the credit-card float

Given what I have to say about the vagaries of consumer debt, you may think that I’m always against using credit cards. Actually, I have credit cards, and I use them — but I pay my balance in full each month. Besides the convenience credit cards offer me — in not having to carry around other forms of payment such as extra cash and checks — I receive another benefit: I have free use of the bank’s money until the time the bill is due. (Some cards offer other benefits, such as frequent flyer miles or other rewards, and I have those types of cards too. Also, purchases made on credit cards may be contested if the sellers of products or services don’t stand behind what they sell.)When you charge on a credit card that does not have an outstanding balance carried over from the prior month, you typically have several weeks (known as the grace period) from the date of the charge to the time when you must pay your bill. This is called playing the float. Had you paid for this purchase by cash or check, you would have had to shell out your money sooner.

If you have difficulty saving money and plastic tends to break your budget, forget the float and reward’s games. You’re better off not using credit cards. The same applies to those who pay their bills in full but spend more because it’s so easy to do so with a piece of plastic.