Bitcoin and other minable cryptocurrencies rely on miners to maintain their network. By solving math problems and providing consent on the validity of transactions, miners support the blockchain network, which will otherwise collapse. For their service to the network, miners are rewarded with newly created cryptocurrencies (such as Bitcoins) and transaction fees.

To really understand mining, you first need to explore the world of blockchain technology. Here’s a quick overview: If you want to help update the ledger (transaction record) of a minable cryptocurrency like Bitcoin, all you need to do is guess a random number that solves a math equation. Of course, you don’t want to guess these numbers all by yourself. That’s what computers are for! The more powerful your computer is, the more quickly you can solve these math problems and beat the mining crowd.

The more you win the guessing game, the more cryptos you receive as a reward. If all of the miners use a relatively similar type of computing power, the laws of probability dictate that the winner isn’t likely to be the same miner every time. But if half of the miners have regular commercial computers while the other half use supercomputers, then the participation gets unfair to the favor of the super powerful computers. Some argue that those with supercomputers will win most of the time, if not all the time.

Cryptocurrency networks such as Bitcoin automatically change the difficulty of the math problems depending on how fast miners are solving them. This process is also known as adjusting the difficulty of the proof-of-work (PoW).

In the early days of Bitcoin, when the miners were just a tiny group of computer junkies, the proof-of-work was very easy to achieve. In fact, when Satoshi Nakamoto released Bitcoin, he/she/it intended it to be mined on computer CPUs. (The true identity of Satoshi is unknown, and I’m adding “it” because there are even discussions that Satoshi can be a government entity.) Satoshi wanted this distributed network to be mined by people distributed around the world using their laptops and personal computers. Back in the day, you were able to solve rather easy guessing games with a simple processor on your computer.

As the mining group got larger, so did the competition. After a bunch of hard-core computer gamers joined the network, they discovered the graphics cards for their gaming computers were much more suitable for mining. My husband was sure among those people. As a gaming geek, he had two high-end computers with Nvidia graphic cards sitting in his game room, collecting dust after we got married. (For obvious reasons, he had to trade his gaming time up for dating time.) When he saw my passion for cryptos, he had to jump in and turn on his computers to start mining. But because he joined the mining game rather late, mining Bitcoin wasn’t turning out to be that profitable. That’s why he turned to mining other minable cryptos.

Mining isn’t a get-rich-quick scheme. To mine effectively, you need access to pretty sophisticated equipment. First you need to do the math to see whether the initial investment required to set up your mining assets is going to be worth the cryptos you get in return. And even if you choose to mine cryptocurrencies instead of buying them, you’re still betting on the fact that their value will increase in the future.

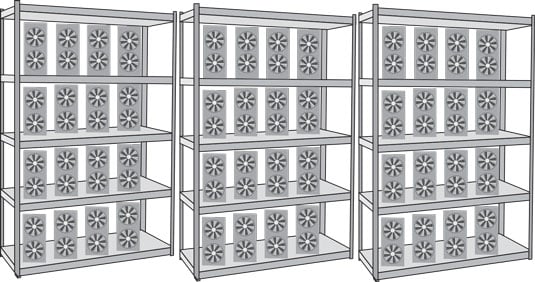

As Bitcoin became more popular, mining it became more popular, and therefore more difficult. To add to the challenge, some companies who saw the potential in Bitcoin value started massive data centers, called mining farms, with ranges of high-end computers whose jobs are only to mine Bitcoins. The figure shows an example of a mining farm setup. High-end computers in a mining farm

High-end computers in a mining farmSo next time you think about becoming a Bitcoin miner, keep in mind who you’re going up against! But don’t get disappointed. You do have a way to go about mining: mining pools.