Cross-industry professional collaboration is a key differentiator among financial advisors. You’ll find little competition in the marketplace for financial advisors who routinely coordinate their activities with other professionals on behalf of their clients. Leverage the power of this key differentiator by letting clients and prospects know that you’re dedicated to partnering with others on their advisory team to optimize their financial success.

Team up with your client

As with any partnership or good relationship, communication is key. Touching base with your clients regularly — on an ongoing basis — is the only way to ensure you’re getting the whole picture. Remind your clients that you and they both want the same thing — a great financial outcome over the course of their and their loved ones’ lives.Tell clients what they need to hear, not what you think they want to hear. The fact is that most clients want to be told what they need to hear. That’s what they’re paying you for. Just be sure to present it without judgment or sarcasm. If you’re telling clients what you think they want to hear instead of what they need to hear, you’re enabling bad habits. Your job is to lead your clients in the direction of financially healthier decisions and behaviors.

Your client has hired you because she can’t see the forest for the trees, and you can. If she knows that you’re in partnership together to achieve the same agreed-upon goals, then teamwork will come naturally. Your client will be more open, responsive, and engaged. She’ll understand that she’s better off working with you than trying to manage her finances by herself or with another financial advisor who’s less committed to teamwork.As with any partnership or team, your relationship with a client may encounter some friction and frustration. Even the closest teammates and partners can butt heads and engage in heated debates over what’s best. Usually, they have the same goal; they just disagree over the best way to achieve it. Not only are disagreements completely normal, but they’re also to be expected and can be quite productive. With every disagreement, you and your client glean more about each other, which ideally leads to a deeper relationship with greater understanding.

Partner with your client’s lawyer

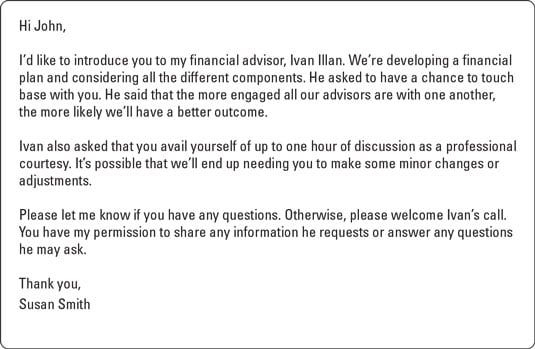

The easiest way to connect with your client’s lawyer is to have your client introduce you via email. This also serves as a written notice, which lawyers like to have to ensure they have permission to discuss client-specific information with another party.To simplify the task for your client, write the introduction yourself and email it to your client to use. The figure is a sample introductory email that your client can send to her lawyer:

A sample introductory email.

A sample introductory email.Work with your client’s accountant

Your client’s accountant can be helpful in the area of tax planning by providing you with your client’s effective tax rate along with an overview of your client’s income and any ideas on how the two of you can work together to ease your mutual client’s tax burden.Accountants are less formal to deal with than lawyers, but you should still ask your client to introduce you via email and provide permission to share information and answer questions.

Host a brainstorming session with your client’s accountant to freely discuss ideas or strategies that she may have leveraged with other clients.

In general, business owners have more complicated tax planning concerns than do salaried employees, so if your client owns a business, having a tax advisor on the team is a big plus. During your initial conversation with your client’s tax accountant, here are a few tax-savings strategies for business owners that you may want to discuss to get the ball rolling:- Changing the client’s business structure: Business structure (sole proprietorship, C-corporation, S-corporation, LLC) impacts the way the business owner gets paid, which can affect income taxes and the amount of self-employment tax (FICA) your client pays.

- Establishing a profit-sharing retirement plan: Profit sharing retirement plans enable businesses to contribute a portion of the business’s profits into an employee retirement account that grows tax-free. In addition, contributions made by the business aren’t included in the business’s taxable income. In a family business, this can be a great way to build wealth for family members who work in the business.

- Using fringe benefit plans for employees: Fringe benefits include group life, health, and disability insurance; dependent care; and tuition reimbursement. They’re a great way for employers to improve employee recruitment and retention by adding compensation that provides tax breaks for the business. For example, employee health insurance premiums paid by the business are generally tax-deductible.

- Using an accountable plan: An accountable plan governs how a business reimburses employees for business expenses. Under such a plan, reimbursements to an employee or business owner aren’t included as part of the employee or owner’s income, but the business can take a deduction for these amounts.

Work on your follow-through with the financial advisory team

Nothing is more embarrassing than going through all the time and effort to collaborate with other advisors for a client’s benefit only to lose track of who’s doing what next. To avoid such embarrassments, get organized and follow through on whatever the team discussed.Set deadlines in your communications with other advisors and your clients. Create reminders in your customer relationship management (CRM) software or whatever scheduling tool you use. Collaborations can take considerable time to come to fruition, and everyone can easily lose track when they get busy with other things. I’ve had projects go on for a year or two before we finally proceeded to implement the plan.

The more complicated the client’s needs and the more advisors are involved on a project, the longer the process takes. Don’t be discouraged; it’s a natural side effect of going up-market in your client acquisition.