A direct materials variance results from one of two conditions: differences in the prices paid for materials or discrepancies in the quantities used in production. To find these variances, you can use formulas or a simple diagram approach.

Using formulas to calculate direct materials variances

The total direct materials variance is comprised of two components: the direct materials price variance and the direct materials quantity variance.

To compute the direct materials price variance, take the difference between the standard price (SP) and the actual price (AP), and then multiply that result by the actual quantity (AQ):

Direct materials price variance = (SP – AP) x AQ

To get the direct materials quantity variance, multiply the standard price by the difference between the standard quantity (SQ) and the actual quantity:

Direct materials quantity variance = SP x (SQ – AQ)

The total direct materials variance equals the difference between total actual cost of materials (AP x AQ) and the budgeted cost of materials, based on standard costs (SP x SQ):

Total direct materials variance = (SP x SQ) – (AP x AQ)

For example, Band Book’s standard price is $10.35 per pound. The standard quantity per unit is 28 pounds of paper per case. This year, Band Book made 1,000 cases of books, so the company should have used 28,000 pounds of paper, the total standard quantity (1,000 cases x 28 pounds per case). However, the company purchased 30,000 pounds of paper (the actual quantity), paying $9.90 per case (the actual price).

Based on the given formula, the direct materials price variance comes to a positive $13,500, a favorable variance:

Direct materials price variance = (SP – AP) x AQ = ($10.35 – $9.90) x 30,000 = $13,500 favorable

This variance means that savings in direct materials prices cut the company’s costs by $13,500.

The direct materials quantity variance focuses on the difference between the standard quantity and the actual quantity, arriving at a negative $20,700, an unfavorable variance:

Direct materials quantity variance = SP x (SQ – AQ) = $10.35 x (28,000 – 30,000) = –$20,700 unfavorable

This result means that the 2,000 additional pounds of paper used by the company increased total costs $20,700. Now, you can plug both parts in to find the total direct materials variance. Compute the total direct materials variance as follows:

Total direct materials variance = (SP x SQ) – (AP x AQ) = ($10.35 x 28,000) – ($9.90 x 30,000) = $289,800 – $297,000 = –7,200 unfavorable

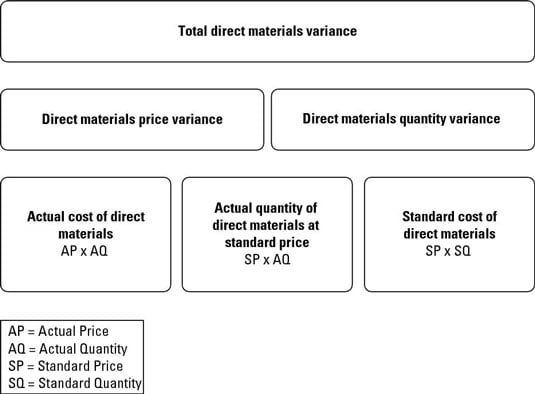

Diagramming direct materials variances

The following figure provides an easier way to compute price and quantity variances. To use this diagram approach, just compute the totals in the third row: actual cost, actual quantity at standard price, and the standard cost.

The actual cost less the actual quantity at standard price equals the direct materials price variance. The difference between the actual quantity at standard price and the standard cost is the direct materials quantity variance. The total of both variances equals the total direct materials variance.

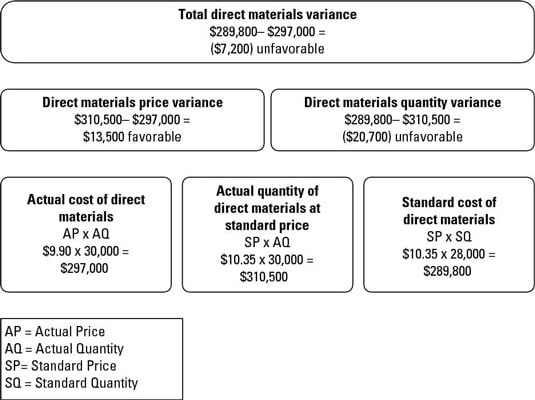

To apply this method to the Band Book example, take a look at the next diagram. Start at the bottom. Direct materials actually cost $297,000, even though the standard cost of the direct materials is only $289,800. The actual quantity of direct materials at standard price equals $310,500.

To compute the direct materials price variance, subtract the actual cost of direct materials ($297,000) from the actual quantity of direct materials at standard price ($310,500). This difference comes to a $13,500 favorable variance, meaning that the company saves $13,500 by buying direct materials for $9.90 rather than the original standard price of $10.35.

To compute the direct materials quantity variance, subtract the actual quantity of direct materials at standard price ($310,500) from the standard cost of direct materials ($289,800), resulting in an unfavorable direct materials quantity variance of $20,700. Because the company uses 30,000 pounds of paper rather than the 28,000-pound standard, it loses an additional $20,700.

This setup explains the unfavorable total direct materials variance of $7,200 — the company gains $13,500 by paying less for direct materials, but loses $20,700 by using more direct materials.