Two methods are available to prepare a statement of cash flows: the indirect and direct methods. The Financial Accounting Standards Board (FASB) prefers the direct method, while many businesses prefer the indirect method. Regardless of which method you use, the bottom-line cash balance is the same, and it has to equal the amount of cash you show on the balance sheet.

The last step in compiling the statement of cash flows is to verify that the ending balance in the cash flow statement equals the ending balance in the cash account on the balance sheet. If they don’t agree, there must be a mistake or missing cash transactions in the cash flow statement. This is the process used for both the direct and indirect method.

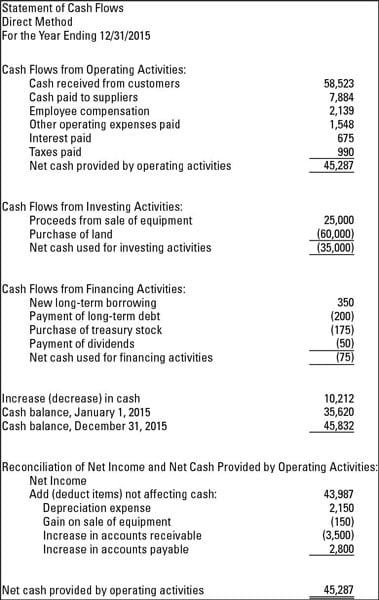

The following figures show you what the statement of cash flows looks like when you use both the direct and indirect methods of preparation. The following figure is the statement of cash flows using the direct method.

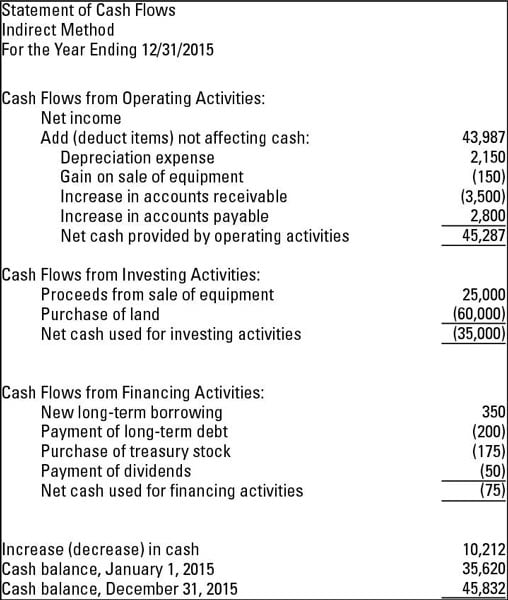

The next figure is the statement of cash flows using the indirect method. As you look at both, note that the cash balance on 12/31/2015 is the same for both methods.

Using the direct method

The direct method of preparing the statement of cash flows shows the net cash from operating activities. This section shows all operating cash receipts and payments. Some examples of cash receipts you use for the direct method are cash collected from customers, as well as interest and dividends the company receives. Examples of cash payments are cash paid to employees and other suppliers and interest paid on notes payable or other loans.

Here are three key facts to remember about the direct method:

You present cash received and paid — not net income or loss as shown on the income statement.

Any differences between the direct versus the indirect method are located in the operating section of the statement of cash flows. The financing and investing sections are the same regardless of which method you use.

The FASB prefers the direct method because it believes the direct method gives the users of the financial statements a more complete picture of the health of the business.

Starting indirectly with net income

When you use the indirect method of preparing the statement of cash flows, the operating section starts with net income from the income statement. You then adjust net income for any noncash items hitting the income statement. One typical adjustment is for depreciation, which is a noncash transaction.

Other common items requiring adjustment are gains and losses from the sale of assets. This is because the gains or losses shown on the income statement for the sale will rarely if ever equal the cash a company receives.

In other words, gain or loss is based on the difference between the asset’s net book value, which is cost less accumulated depreciation, and the amount the item sold for — not how much cash the buyer hands over to the seller.

Assume a business has a machine it no longer uses. Because it no longer needs the machine, the business sells it to another company for $1,500. The cash received is $1,500, but what about gain or loss on disposal? Consider these facts:

The company originally paid $3,000 to purchase and install the machine.

The asset was depreciated, meaning that the asset’s cost was gradually posted to depreciation expense over the machine’s useful life. The total amount depreciated over time (accumulated depreciation) was $2,000.

Book value for the machine on the date of sale was $1,000 ($3,000 cost – $2,000 accumulated depreciation).

The company debits (increases) cash for $1,500 and debits (reduces) accumulated depreciation for $2,000. When the asset is sold, the accumulated depreciation account is adjusted to zero. Debits total $3,500.

The asset is credited (reduced) by $3,000, which is the original cost.

Gain on disposal is a credit for $500, which is the difference between $3,500 total debit and the $3,000 credit. After the gain is posted, total debits and credits both equal $3,500.

You see that the cash received ($1,500) differs from the gain on disposal ($500). These are the types of transactions that are reconciled in the statement of cash flows. The net income change ($500 gain) doesn’t match the $1,500 cash inflow.