A business has its choice between two quite different methods of reporting cash flow from operating activities in its statement of cash flows. Financial reporting standards permit either approach — the direct method (which is the preferred method) or the indirect method.

The direct method for reporting cash flow

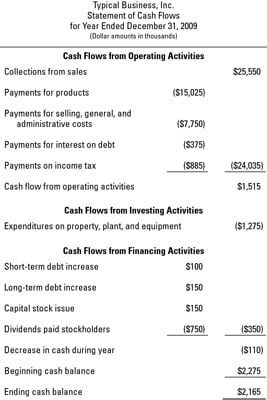

What you see in the first section of the statement of cash flows in the following figure is called the direct method for reporting cash flow from operating activities. The term “direct” is probably meant to refer to the cash flows connected with sales and expenses. For example, the business collects $25.55 million from customers during the year, which is the direct result of making sales.

When issuing the financial reporting standard for the statement of cash flows, the Financial Accounting Standards Board (FASB) thought that financial report readers would compare cash flow from operating activities with net income, and they would want some sort of explanation for the difference between these two important financial numbers.

Therefore, the FASB decreed that the statement of cash flows should also include a reconciliation schedule to explain the difference between cash flow from operating activities and net income. Or, a business can use the alternative method for reporting cash flow from operating activities.

The indirect method for reporting cash flow

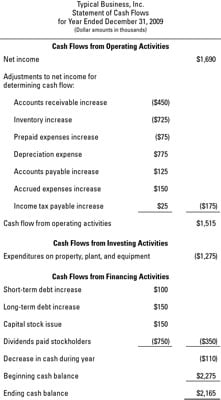

The alternative method for reporting cash flow from operating activities starts with net income, and then makes adjustments in order to reconcile cash flow from operating activities with net income. This method is called the indirect method, shown in the next figure.

The indirect method for reporting cash flow from operating activities focuses on the changes during the year in the assets and liabilities that are connected with sales and expenses.

While there are obvious differences in the first section of the statement of cash flows between the two methods for reporting cash flow from operating activities, the other two sections of the statement (cash flow from investing activities and cash flow from financing activities) are the same.

The level of detail disclosed in these two sections varies from business to business. For example, some companies report one aggregate amount for all capital expenditures (investments in new long-term operating assets), whereas others give a more detailed breakdown.