A sole proprietorship is a business that has only one owner. As the individual in charge of the whole shooting match, the single owner has complete control and decision-making power over the business. Owners aren’t classified as employees.

Sole proprietorships aren’t all moonlight and magnolias, however. The sole proprietor is personally liable for the debts and obligations of the business. Additionally, this risk extends to any liabilities incurred as a result of acts committed by employees of the company. Funding is usually by the owner rather than outside investors.

No real legal distinction is made between the owner and the business, so it’s an inexpensive type of entity to start up and maintain. Few formal business requirements and minimal legal costs are involved in forming a sole proprietorship.

In most jurisdictions of the United States, the only legal requirement is that the sole proprietorship have adequate business licensing with the state, city, and county in which it operates.

The equity section of the balance sheet of a sole proprietorship contains two accounts:

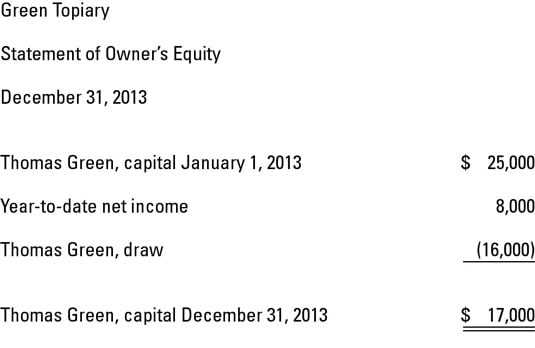

Owner capital is the amount of money the sole proprietor invests in the business.

Owner withdrawals represent distributions the owner makes to him- or herself.

Some sole proprietorships use a retained earnings account to hold income transactions.