Here are the four largest (and most popular with retail investors): the Federal National Mortgage Association (Fannie Mae), the Federal Home Loan Mortgage Corporation (Freddie Mac), the Federal Home Loan Banks (FHLB), and the Government National Mortgage Association (GNMA or Ginnie Mae).

How big is a big agency?

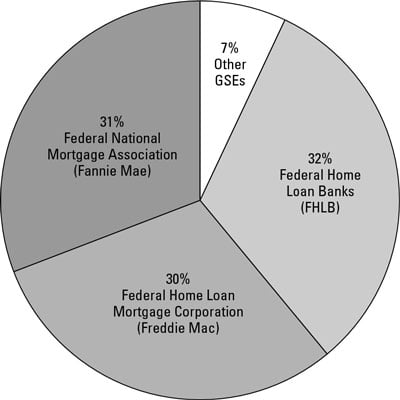

Many GSEs exist, but as the figure shows, Fannie Mae, Freddie Mac, and FHLB issue the vast majority of non-mortgage-backed bonds (sometimes referred to as debentures). The percentages reflected in this figure, which are for 2010, were supplied by the Securities Industry and Financial Markets Association (SIFMA).

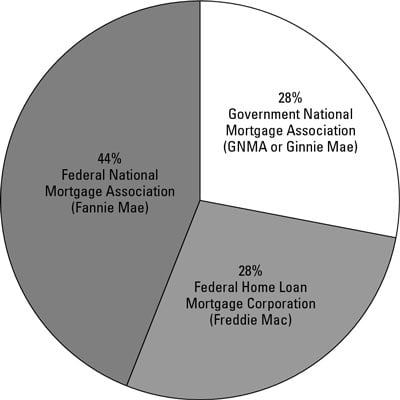

And as the next figure shows, more than 95 percent of all mortgage-backed securities issued in the United States are issued by Fannie Mae, Freddie Mac, and Ginnie Mae. Again, the percentages reflected in the figure, which are for 2010, were supplied by the Securities Industry and Financial Markets Association (SIFMA).

Federal National Mortgage Association (Fannie Mae)

Fannie Mae, founded in 1938 but incorporated as a publicly traded company in 1968, raises money by selling bonds. It then turns some of that money over to banks. The banks use the money to make loans, mostly to homebuyers. A sizeable chunk of all home loans in America are either owned or guaranteed by Fannie Mae or its close cousin, Freddie Mac.

Most Fannie Mae bonds (generally available in increments of $1,000) are purchased by institutions: insurance companies, other nation’s central banks (especially China’s), university endowments, and so on. But individual investors are certainly welcome to join in the fun, too. The agency issues bonds of varying maturities, and there’s a large secondary market where you can find any maturity from several months to many years down the pike.

Fannie Mae sounds like a public agency, but it’s really a private corporation. That private corporation, like all GSEs, was under government oversight until the housing-market collapse and subprime mortgage fiasco of several years ago. Fannie Mae’s losses were so great that the government placed the company under conservatorship. For all intents and purposes, Fannie Mae is now operating as an official arm of the government.

The takeover meant misery for those who held stock in the private company, but for Fannie Mae bondholders, the government takeover wasn’t a bad thing. In fact, it made the bonds perhaps even safer for those investors.

If you believe that agency debt belongs in your portfolio (it certainly isn’t a necessity but is a good option for many investors), Fannie Mae bonds may be an okay choice. You may want to see what happens with Fannie Mae in the near future. But even if the agency moves ahead to operate as it has in the past (presumably being more careful about taking on too many subprime mortgages), the desirability of the bonds will still depend on the price your broker offers you.

Federal Home Loan Mortgage Corporation (Freddie Mac)

Just like Fannie Mae, this agency is technically a private corporation tied to the government. It was formed in 1970. And like Fannie Mae, Freddie Mac recently fell on hard times, too. In September 2008, the corporation was placed under the control of the Federal Housing Finance Agency. Stockholders were stung, but bondholders fared perfectly fine (as often happens in times of turmoil).

Freddie Mac offers a multitude of bond issues with many maturities, denominations of $1,000, and a choice of traditional or mortgage-backed.

Freddie Mac buys one residential mortgage every few seconds and, by doing so, helps to finance one in six homes in the United States. Most of the mortgages are purchased from primary lenders (such as your neighborhood bank). With the money these lenders get from Freddie Mac, they can go out and make more loans.

Like Fannie Maes, most Freddie Macs are bought by institutions. And as with Fannies, you may want some Freddies in your portfolio, but they aren’t a necessity, and you don’t want to buy them willy-nilly.

Federal Home Loan Banks

The FHLB is not a single agency but a coalition of 12 regional banks formed in 1932. Its mission is to fund low-income housing and housing projects. The money used for the funding comes from — you guessed it — selling bonds. Lots of bonds.

This coalition, considered a government-sponsored enterprise (GSE), is the largest issuer of so-called agency debenture bonds. These bonds are a bit more popular with individual investors than Freddies and Fannies — as well they should be, at least for those in higher tax brackets: The interest earned is exempt from state and local taxes.

Like Fannies and Freddies, FHLB bonds come in many different flavors as far as denominations and maturities.

Government National Mortgage Association (GNMA or Ginnie Mae)

Very much unlike Freddie Mac and Fannie Mae, Ginnie Mae — founded in 1968 to promote home ownership — was, and has always been, a fully owned government corporation. As such, Ginnie Mae bonds have always had the full faith and credit guarantee of Uncle Sam.

Ginnie Mae bonds also differ from Freddie Mac and Fannie Mae bonds, as well as FHLB bonds, in that all Ginnie Maes bonds to date have been mortgage-backed. A pool of mortgages is the meat behind each GNMA bond.

When you buy the bond, your money is passed along to help buy someone’s house. But Ginnie Mae doesn’t actually create the bonds, nor does it actually sell any mortgages. Instead, certain banks are authorized to do that under Ginnie Mae’s approval and guarantee.

Your investment in these bonds is then passed along to potential homebuyers in the form of affordable loans. In other words, Ginnie Mae is like Good Housekeeping. Its seal of approval and guarantee (for which banks pay good money) assure you, the bondholder, that you aren’t going to get stuck with the same kind of mortgage bonds — backed by a whim and a prayer — that helped to sink Lehman Brothers.