When sales are made on store credit, you must record specific information into the accounting system. In addition to entering information regarding cash receipts, you update the customer accounts to be sure each customer is billed and the money is collected. You debit the Accounts Receivable account, an asset account shown on the Balance Sheet, which shows money due from customers.

Here’s how a journal entry of a sale made on store credit looks:

| Debit | Credit | |

|---|---|---|

| Accounts Receivable | $84.80 | |

| Sales | $80.00 | |

| Sales Tax Collected | $4.80 | |

| Cash receipts for April 25 |

In addition to making this journal entry, you enter the information into the customer’s account so that accurate bills can be sent out at the end of the month. When the customer pays the bill, you update the individual customer’s record to show that payment has been received and enter the following into the bookkeeping records:

| Debit | Credit | |

|---|---|---|

| Accounts Receivable | $84.80 | |

| Sales | $84.80 | |

| Payment from S. Smith on Invoice 123. |

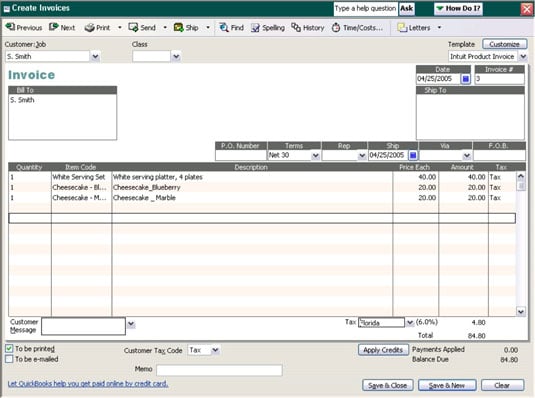

If you’re using QuickBooks, you enter purchases on store credit using an invoice form like the one in the following figure. Most of the information on the invoice form is similar to the sales receipt form, but the invoice form also has space to enter a different address for shipping (the “Ship To” field) and includes payment terms (the “Terms” field).

QuickBooks uses the information on the invoice form to update the following accounts:

Accounts Receivable

Inventory

The customer’s account

Sales Tax Collected

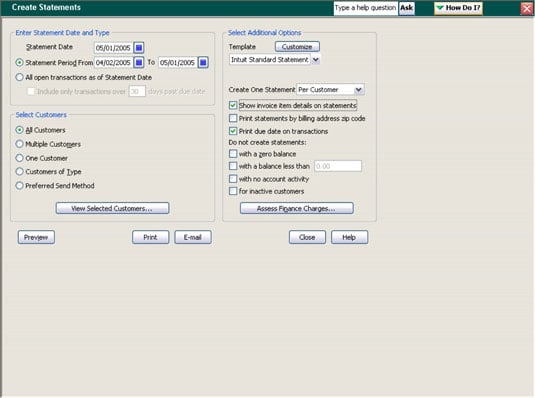

Based on this data, when it comes time to bill the customer at the end of the month, with a little prompting from you (see the next figure), QuickBooks generates statements for all customers with outstanding invoices. You can easily generate statements for specific customers or all customers on the books.

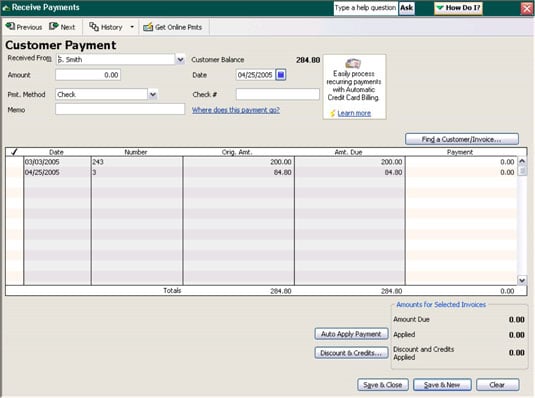

When you receive payment from a customer, here’s what happens:

1. You enter the customer’s name on the customer payment form (shown in the next figure).

2. QuickBooks automatically lists all outstanding invoices.

3. You select the invoice or invoices paid.

4. QuickBooks updates the Accounts Receivable account, the Cash account, and the customer’s individual account to show that payment has been received.

If your company uses a point of sale program that’s integrated into the computerized accounting system, recording store credit transactions is even easier for you. Sales details feed into the system as each sale is made, so you don’t have to enter the detail at the end of day. These programs save a lot of time, but they can get very expensive — usually at least $400 for just one cash register.

Even if customers don’t buy on store credit, point of sale programs provide businesses with an incredible amount of information about their customers and what they like to buy. This data can be used in the future for direct marketing and special sales to increase the likelihood of return business.