Amortization mimics depreciation because you use it to move the cost of intangible assets from the balance sheet to the income statement. Most intangibles are amortized on a straight-line basis using their expected useful life.

Intangible assets have either a limited life or an indefinite life. Limited means the intangible asset won’t be useful forever. For example, the U.S. government grants patent protection for a period of 20 years. Unless the patent has become obsolete, that term is probably the expected useful life the business uses.

Indefinite means no factors affect how long the intangible asset will provide use to the company. You don’t amortize indefinite life intangible assets.

To eventually move the cost off the balance sheet, test indefinite life intangibles at least annually for impairment, which means the carrying cost of the intangible is no longer recoverable.

The second class of intangibles, goodwill, is never amortized. Financial accountants test it yearly for impairment, which means they see whether any worthless goodwill needs to be written off.

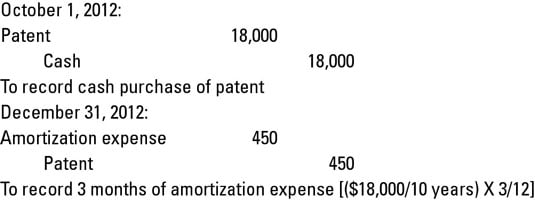

To bring this all home, consider a common intermediate accounting homework assignment involving amortization. Here are your facts and circumstances for this assignment:

On October 1, 2012, Green Inc. purchases a patent from an inventor for $18,000. Green reckons the patent has a useful life of 10 years. The following figure shows how to account for this transaction and amortization expense on December 31, 2012.

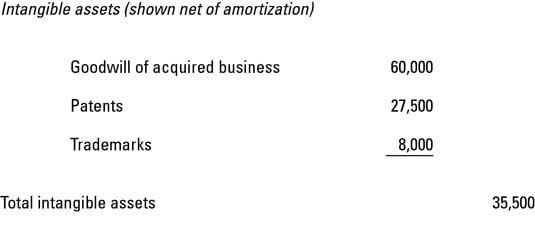

The following figure shows a typical balance sheet intangible section. This section normally shows up on the balance sheet after PP&E.

Accumulated amortization is sometimes used. Most companies are permitted to take the credit directly to the intangible asset account.