Trying to read a balance sheet without having a grasp of its parts on a financial report is a little like trying to translate a language you've never spoken — you may recognize the letters, but the words don't mean much. Unlike a foreign language, however, a balance sheet is pretty easy to get a fix on as soon as you figure out a few basics.

Dig into dates

The first parts to notice when looking at the financial statements are the dates indicated at the top of the statements. You need to know what date or period of time the financial statements cover. This information is particularly critical when you start comparing results among companies. You don't want to compare the 2012 results of one firm with the 2011 results of another.

Economic conditions certainly vary, and the comparison doesn't give you an accurate view of how well the companies competed in similar economic conditions.

On a balance sheet, the date at the top is written after “As of,” meaning that the balance sheet reports a company's financial status on that particular day. A balance sheet differs from other kinds of financial statements, such as the income statement or statement of cash flows, which show information for a period of time such as a year, a quarter, or a month.

If a company's balance sheet states “As of December 31, 2012,” the company is most likely operating on the calendar year. Not all firms end their business year at the end of the calendar year, however. Many companies operate on a fiscal year instead, which means they pick a 12-month period that more accurately reflects their business cycles.

For example, most retail companies end their fiscal year on January 31. The best time of year for major retail sales is during the holiday season and post-holiday season, so stores close the books after those periods end.

To show you how economic conditions can make comparing the balance sheets of two companies difficult during two different fiscal years, consider an example surrounding the terrorist attacks on September 11, 2001.

If one company's fiscal year runs from September 1 to August 31 and another's runs from January 1 to December 31, the results may be very different. The company that reports from September 1, 2000, to August 31, 2001, wasn't impacted by that devastating event on its 2000/2001 financial reports.

Its holiday season sales from October 2000 to December 2000 are likely much different from those of the company that reports from January 1, 2001, to December 31, 2001, because those results include sales after September 11, when the economy slowed considerably. However, the first company's balance sheet for September 1, 2001, to August 31, 2002, shows the full impact of the attacks on its financial position.

Nail down the numbers

As you start reading the financial reports of large corporations, you see that they don't use large numbers to show billion-dollar results (1,000,000,000) or carry off an amount to the last possible cent, such as 1,123,456,789.99. Imagine how difficult reading such detailed financial statements would be!

At the top of a balance sheet or any other financial report, you see a statement indicating that the numbers are in millions, thousands, or however the company decides to round the numbers. For example, if a billion-dollar company indicates that numbers are in millions, you see 1 billion represented as 1,000 and 35 million as 35. The 1,123,456,789.99 figure would appear as 1,123.

Rounding off numbers makes a report easier on the eye, but be sure you know how companies are rounding their numbers before you start comparing financial statements among them. This issue is particularly crucial when you compare a large company with a smaller one. The large company may round to millions, whereas the smaller company may round to thousands.

Format

Balance sheets come in three different styles: the account format, the report format, and the financial position format. Here’s a sample of each format.

Account format

The account format is a horizontal presentation of the numbers.

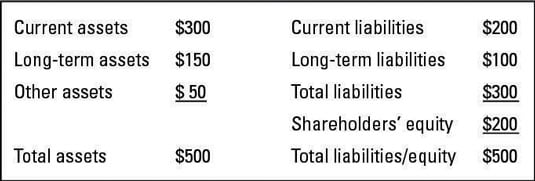

A balanced sheet shows total assets equal to total liabilities/equity.

Report format

The report format is a vertical presentation of the numbers.

Financial position format

Companies in the U.S. rarely use the financial position format, although it is common internationally, especially in Europe. The key difference between this format and the other two is that it has two lines that don’t appear on the account and report formats:

Working capital: This line indicates the current assets the company has available to pay bills. You find the working capital by subtracting the current assets from the current liabilities.

Net assets: This line shows what’s left for the company’s owners after all liabilities have been subtracted from total assets.

(Keep in mind that noncurrent assets are long-term assets as well as assets that aren’t current but also aren’t long term, such as stock ownership in another company.)

As investing becomes more globalized, you may start comparing U.S. companies with foreign companies. Or perhaps you are considering buying stock directly in European or other foreign companies. You need to become more familiar with the financial position format if you want to read reports from foreign companies.