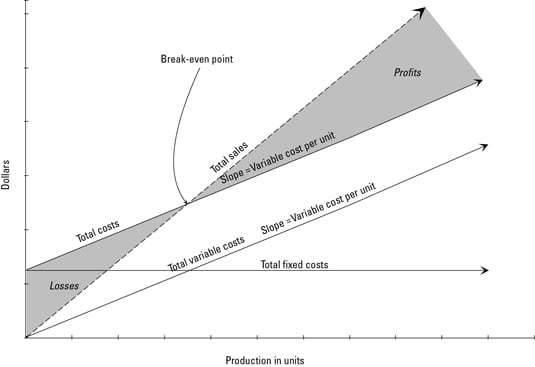

Managerial accounting provides useful tools, such as cost-volume-profit relationships, to aid decision-making. Cost-volume-profit analysis helps you understand different ways to meet your company’s net income goals. This image describes the relationship among sales, fixed costs, variable costs, and net income:

-

The bottom axis indicates the level of production — the number of units you make.

-

The left axis indicates value in dollars.

-

Where total sales equals total costs, the company breaks even (which is why that’s called the break-even point).

-

The shaded area to the upper right of this break-even point is profit.

-

The shaded region to the lower left is net loss.

-

Total variable costs are a diagonal line because the higher the production, the greater the variable costs.

-

The total fixed costs line is horizontal because regardless of the production level, fixed costs stay the same.

-

Total costs equal the sum of total variable costs and total fixed costs.