When you prepare financial statements at the end of an accounting period, you may need to adjust the books to allow for bad debts from customers that will never pay the amount owed to your business. No company likes to accept the fact that it will never see the money owed by some of its customers, but, in reality, that’s what happens to most companies that sell items on store credit.

When your company determines that a customer who has bought products on store credit will never pay for them, you record the value of that purchase as a bad debt.

At the end of an accounting period, you should list all outstanding customer accounts in an aging report. This report shows which customers owe how much and for how long. After a certain amount of time, you have to admit that some customers simply aren’t going to pay.

Each company sets its own determination of how long it wants to wait before tagging an account as a bad debt. For example, your company may decide that when a customer is six months late with a payment, you’re unlikely to ever see the money.

After you determine that an account is a bad debt, you should no longer include its value as part of your assets in Accounts Receivable. Including its value doesn’t paint a realistic picture of your situation for the readers of your financial reports. Because the bad debt is no longer an asset, you adjust the value of your Accounts Receivable to reflect the loss of that asset.

You can record bad debts in a couple of ways:

By customer: Some companies identify the specific customers whose accounts are bad debts and calculate the bad debt expense each accounting period based on customers accounts.

By percentage: Other companies look at their bad-debts histories and develop percentages that reflect those experiences. Instead of taking the time to identify each account that will be a bad debt, these companies record bad debt expenses as a percentage of Accounts Receivable.

You need to prepare an adjusting entry at the end of each accounting period to record bad debt expenses. Here’s an adjusting entry to record bad debt expenses of $1,000:

| Debit | Credit | |

|---|---|---|

| Bad Debt Expense | $1,000 | |

| Accounts Receivable | $1,000 | |

| To write off customer accounts. |

You can’t have bad debt expenses if you don’t sell to your customers on store credit. You only need to worry about bad debt if you offer your customers the convenience of buying your products on store credit.

If you use a computerized accounting system, check the system’s instructions for how to write off bad debts. To write off a bad debt using QuickBooks:

Open the screen where you normally record customer payments, and instead of entering the amount received in payment, enter “$0.”

Place a check mark next to the amount being written off.

Click Discount and Credits at the bottom-right part of the screen to open that window and see the amount due.

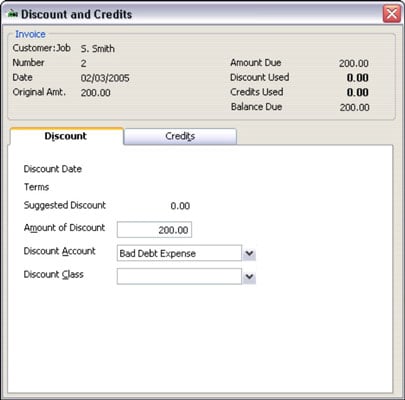

On the Discount tab, which is shown in the following figure, type in the amount of the discount.

In QuickBooks, you record bad debts on the Discount and Credits page, which is part of the Customer Payment function.

In QuickBooks, you record bad debts on the Discount and Credits page, which is part of the Customer Payment function.Select Bad Debt Expense from the Discount Account menu.

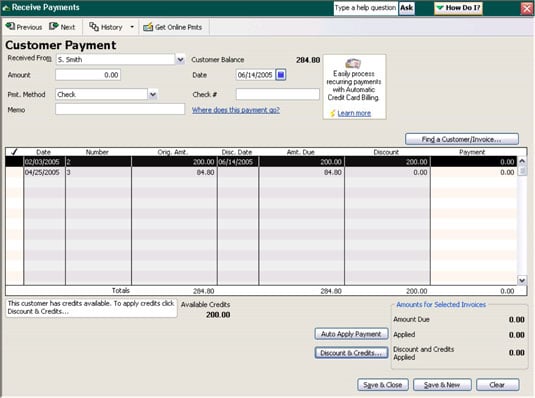

Click Done and verify that the discount is applied and no payment is due (see the figure below).

After you record a bad debt in QuickBooks, the discount appears, indicating that $0 is due.

After you record a bad debt in QuickBooks, the discount appears, indicating that $0 is due.