The three primary financial statements of a business are generally reported in multiyear financial statements, using a two- or three-year comparative format. Generally accepted accounting principles (GAAP) favor presenting these comparative financial statements for private companies, but it is not required.

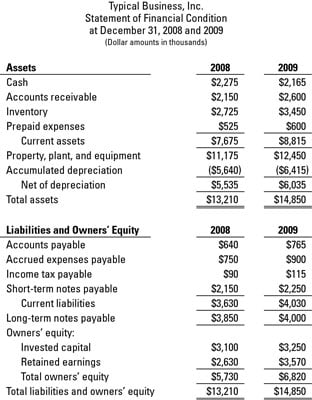

Here's an example of a two-year comparative format for a balance sheet, to give you a sense of what these comparative financial statements might look like:

Two- or three-year comparative financial statements are de rigueur in filings with the Securities and Exchange Commission (SEC). Public companies have no choice, but private businesses are not under the SEC’s jurisdiction.

The main reason for presenting comparative financial statements is for trend analysis. A business’s managers, as well as its outside investors and creditors, are extremely interested in the general trend of sales, profit margins, ratio of debt to equity, and many other vital signs of the business. Slippage in the ratio of gross margin to sales from year to year, for example, is a very serious matter.